Microsoft's Earnings Analysis

Evaluating Microsoft's Cloud Strategy, Gaming Business and Acquisitions

In May 2022, during Microsoft’s developer conference called “Microsoft Build”, Satya reminded us that when Microsoft was founded 47 years ago it was a time of both great opportunity and crisis. Today, we are in a similar environment. We are seeing macroeconomic headwinds with a recession looming. At the same time, the job market and spending have remained high considering the interest rates and inflation.

In today’s essay, I want to write about Microsoft’s Q4 2022 performance. I will also touch upon Nauance’s and Xandr's acquisition, and explain what is happening there. Talk about declining gaming revenue and the Activision Blizzard acquisition.

Before we move ahead, I want to disclose that I have a long position with Microsoft. But this analysis is independent of my investment.

Earnings Summary - Q4 FY’22

Q4 Revenues increased by 12% to $51.9B. For the full fiscal year 2022, Microsoft’s revenue is $198.3B up 18%, with EPS of $9.65, up 20% YoY.

Q4 Operating income increased by 8% to $20.5B

Q4 Net income increased by 2% to $16.7B

Q4 Operating expenses grew by 14% citing investments in cloud, engineering, LinkedIn, and Nuance.

The biggest growth was in the cloud which grew by 28% YoY and enjoyed a healthy gross margin of 69%.

Q4 Cash flow from operations increased by 8% to $24.6B again driven by strong cloud growth. Free Cash Flow (FCF) was up 9% YoY to $17.8B.

Microsoft closed its fiscal year with 18% revenue growth, the highest since 2008. At the same time, operating margins were at 42% - a two-decade high. This is positive news for wall street analysts who love future guidance to make or break stocks. Microsoft re-affirmed double-digit growth both in revenue and operating income for the new fiscal year. If that happens, it will be Microsoft’s sixth consecutive year of growth.

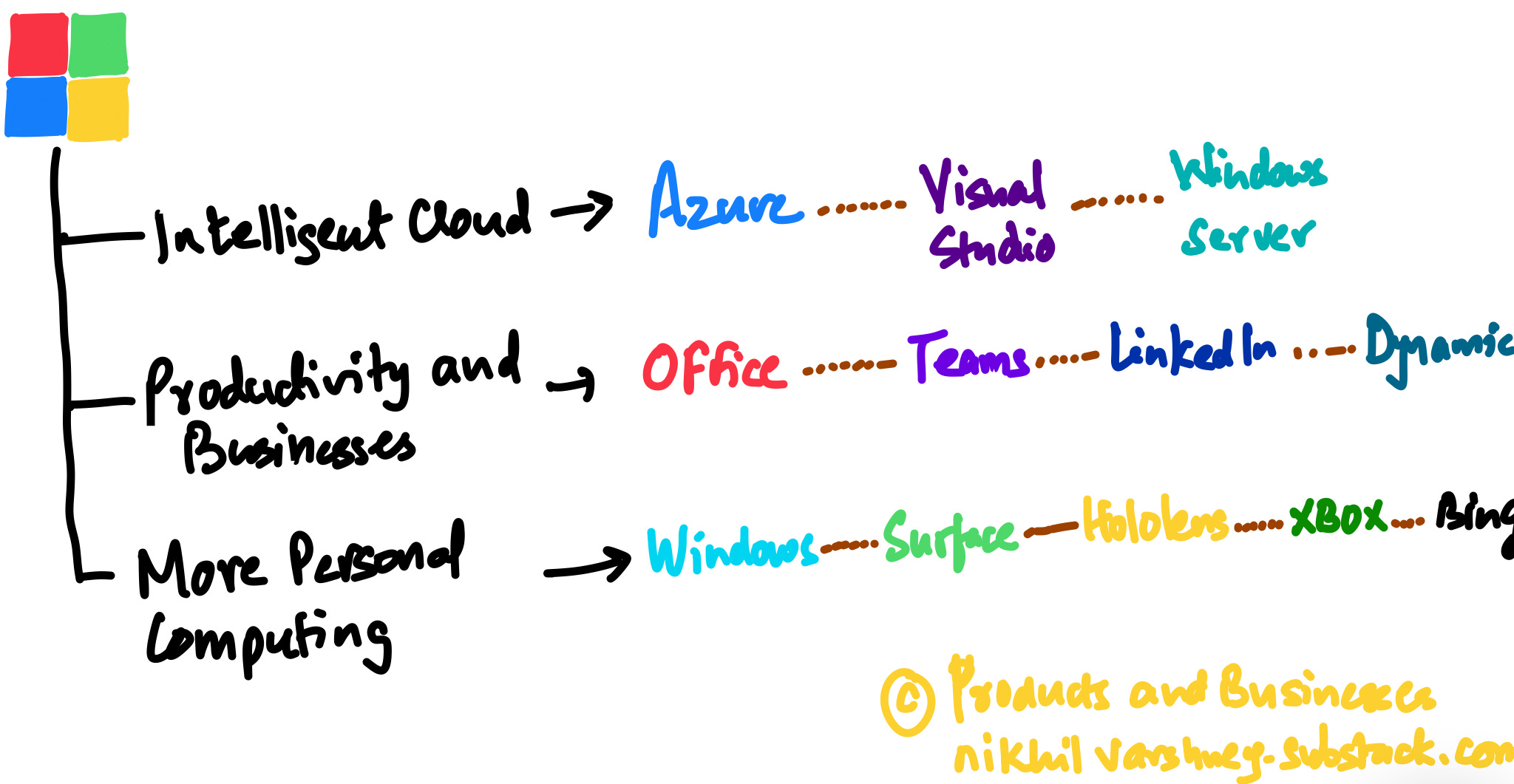

A snapshot of Microsoft’s revenue streams

Below is the review of critical growth sectors for Microsoft. This analysis should help you evaluate Microsoft’s growth prospects.

Cloud Strategy and Tech Stack

Microsoft saw the biggest growth in the intelligent cloud which includes Azure and server products. Even with a tough macroeconomic environment, Microsoft was able to grow this business. From Microsoft blog:

Oracle and Microsoft announced the availability of Oracle Database Service for Microsoft Azure. Earlier this month, we completed the acquisition of Miburo to boost threat intelligence research into new foreign cyber threats, and Netflix announced Microsoft as technology and sales partner for its new consumer subscription plan. P&G has selected Microsoft as its preferred cloud provider to enable scalable predictive maintenance, controlled release, touchless operations and manufacturing sustainability optimization from diapers to paper towels. American Airlines has chosen Microsoft Azure as its preferred cloud platform, applying AI, machine learning and data analytics to reduce time waiting on the runway, saving thousands of gallons of jet fuel per year and giving connecting customers extra time to make their next flights.

With recession looming, companies (big or small) will need to bring down the costs of their products and services. Cloud technology helps cut costs, streamline efficiency and ensure data is available to produce business insights. These opportunities will help fuel the growth of Azure.

Cloud business is supposed to grow at 16% YoY and is expected to reach a trillion dollars by 2026. AWS is a leader in the cloud market with approx 33% market share. Microsoft is second with a 21% market share, and Google on third with a 10% share. What separates Microsoft from other key cloud providers is the Tech Stack. Microsoft states this as:

Ideas —> code —> cloud —> world (customers).

Let us talk about Code and Cloud:

Code

Start with GitHub codespaces, which puts your entire development in the web browser and can be used offline. Alternatively, Microsoft provides Window’s Dev box for developers on PC.

Cloud and AI

Cloud-native apps power rich data and can be infused with AI to improve existing scenarios and introduce new ones. Microsoft has built critical AI models which include Turing (for rich language coding), Z-code (translation across 100s of different languages), and Florence (for visual recognition). In addition, OpenAI (Microsoft’s partner) has models for human-like language generation and DALL-E for realistic image generation.

By building these models in Azure, Microsoft has allowed its customers direct access to this tech and uses these models based on their use cases. This also puts Microsoft in a great position in non-window environments. By being cloud-native, Microsoft is no longer servicing just Windows PCs. It can service all clients and not just the ones it owns.

This is where partnerships with Oracle and Adobe are critical. Cross-platform development is a win for Microsoft. Cloud is not only Microsoft’s growth leader but it also compensates for decelerating segments like Personal Computing.

Gaming and Activision Blizzard

Microsoft’s gaming revenue declined by 7%. Xbox revenue declined by 6%. Xbox suffered from low engagement hours across the board and was also hampered by supply chain issues for consoles. There are headwinds across the gaming industry. This is not Microsoft-specific. Both console and mobile gaming have taken a hit.

Despite the headwinds, Microsoft is in a great spot. Microsoft has put up an all-cash $69B deal to buy Activision (pending regulatory approval). Activision provides Microsoft with $9B in revenue and 370M monthly active users (MAUs). This deal is a move post console world. It's about luring gamers into an ecosystem. Microsoft wants players to go to the hub.

The gaming industry has changed. It is no longer about playing in silos. With Twitch and Discord, gaming is now a tight-knit community. It is social more than ever. Gaming is moving away from console and walled garden war to building a community war.

Microsoft game pass has 25M subscribers. Adding 370M from Activision provides Microsoft with an opportunity to not only increase game pass subscription revenue but also build products and services around its gaming community. Hypothetically speaking, even if Microsoft converts 40% of Activision users to Microsoft game pass subscribers, then that would be $1.5B in monthly or $18B in yearly game pass revenue.

More than the revenues, Microsoft is interested in building a gaming community that can later be sold different products and services such as Metaverse.

Nuance and Xandr Acquisitions

Nuance

Microsoft acquired Nuance for $16B, paying a premium of 23% back in 2021. The deal was finally approved by regulators in March of 2022. Amy Hood, Microsoft’s CFO, stated in 2021 that this deal will enable Microsoft to move into high-growth markets. Nuance at its core is a conversational AI company. But what is interesting about Nuance is its ability to apply AI algorithms to healthcare, telecommunications, and banking. So how has this acquisition panned out?

Money in healthcare tech is from data. Nuance’s DAX (Dragon Ambient eXperience) software enables providers to dictate patients' notes rather than type them out. DAX is now (after acquisition) very deeply integrated with Azure and Teams. With data interoperability regulations where Electronic Health Records (EHRs) are required to communicate with each other, players like Microsoft will get a strong edge.

On top of this, Nuance has put Microsoft directly in the provider-patient conversation loop. Microsoft's strategy with healthcare is patient experience. Unlike Amazon’s which is to reinvent the healthcare processes with PillPack, OneMedical, and other failed attempts such as Haven.

In summary, the Nuance acquisition is still in its infancy and Microsoft is building its strategy to score runs by being patient friendly AI company that uses data to get patients better access to care. There are no positives or negatives about this acquisition at this point. Microsoft has a strategy and we will have to see how this strategy pans out.

Xandr

Microsoft has expanded its feet into advertising. Microsoft has $10B in advertising revenue. To put this into perspective, Twitter has $4.2B and Snap has $3.5B. Whereas Google has $200B and Facebook has $100B. To compete Microsoft is looking to set its footing to capture the pie from an $800B advertising industry.

Xandr can help Microsoft accelerate its understanding of user preferences, technology, and customer base. It will help Microsoft provide a data-driven ad platform.

The advertising industry is seeing a shift in the advertising model from 3rd party cookies model to the first-party integrated advertising. Apple’s App Tracking Tranceparency (ATT) is limiting the use of user data for pushing ads. Xandr provides Microsoft with a “first party, data led advertising solution”.

Microsoft’s ad revenue is spread across search (Bing, Yahoo, DuckDuckGo), LinkedIn, MSN, and Xbox. Xandr provides access to the broader web. The problem for Microsoft is to integrate and stitch all of these pieces together. It will be difficult considering LinkedIn has operated as an independent entity. The good news is Microsoft has time and money to build while other businesses pay the bills.

A recent partnership with Netflix has started to provide fruits to the Xandr acquisition. I wrote about that partnership in detail here.

Conclusion

To conclude, I would just like to quote WSJ. These lines are sufficient to summarize Microsoft’s advantage and why there is a high probability that it will continue to succeed.

Still, Microsoft’s diversity is a relative strength compared with its megacap tech peers. The other four—Apple, Amazon, Google and Facebook—are more than 80% reliant on the singular markets of hardware, retail and advertising respectively. And Microsoft’s areas of strength are mostly likely to hold up best even in a recession.

Cheers