Metaverse and Numbers: Understanding the COST and TAM - Part III of the Metaverse series

TL; DR

Looking back at the shift from Web 1.0 to Web 2.0, there were various cost components tied to Web 2.0 that were all built on Web 1.0. Similarly, there will be significant costs tied to building Web 3.0 upon Web 2.0 infrastructure

Market Cap for metaverse and gaming companies is around ~14T. Expenditure on building the metaverse could reach up to $700B

Different organizations project a different number in the range of $800B to ~$2.6T

According to Markets and Markets report, the Augmented reality (AR) market is supposed to grow from $15.3B to $77B by 2025 at a staggering 38.1% CAGR. Similarly, the Virtual Reality (VR) market is projected to grow from $6.1B to $20.9B in 2025 at a 27% CAGR

The open gaming market has opened up the competition and what has happened since is that it has allowed the business model to shift from upfront fees to more in-game purchases and hence expanded the use of cryptocurrency

JP Morgan estimates the total in-game spending in metaverse will reach $18.41B

What we need are the social attitudes to change to experience this new era on the internet.

Well, here I am writing the third piece of the metaverse series. It feels good to honor this commitment that I had with myself to go the last mile to finish the topic that I started. Since we all are here, let us do a quick recap, shall we? In part 1 – I had written about the fundamentals of the metaverse. I had defined metaverse as

The grand vision of the metaverse is to provide a parallel digital universe connected to our physical world through multiple digital technologies. The convergence of the virtual (online) and real (offline) universes will enable us to communicate in the digital world through avatars

I also talked about the history of the metaverse, and how it all began with Snow Crash and finally we have Facebook renamed as meta to support its metaverse vision.

In part 2 – I wrote about the requirement of the network (bandwidth and latency), hardware (AR/VR, computing power, etc.), and interoperability (different metaverse platforms talking to each other). What I have also understood is that interoperability will play the most crucial role to make the vision of metaverse successful. No one company, be it Facebook, Microsoft, or Roblox, will be able to dominate it and will also not be able to operate in silos. Their platforms will have to talk to each other and allow the transfer of assets (NFTs, crypto, avatars, etc.).

To get going, let us get straight to the point, what will it cost to build the metaverse based on what we know so far. The answer is not that simple. I have tried to understand this phenomenon as blocks in my head. Let’s start with the first block which is to understand the cost of building the metaverse and then subsequently go to other blocks of sizing different metaverse markets.

Cost of building the metaverse

Looking back at the shift from Web 1.0 to Web 2.0, there were various cost components tied to Web 2.0 that were all built on Web 1.0. Similarly, there will be significant costs tied to building Web 3.0 upon Web 2.0 infrastructure. The best way of knowing is to see the costs that Meta Platforms (f.k.a Facebook) is incurring from their balance sheet since they disclosed reality labs results in Feb 2022. Please mind, that disclosing reality lab results led to erasing of $250bn from their market cap in one day. Let us look at different buckets associated with the costs of building the metaverse. (check below Meta 10-K)

We anticipate that additional investments in our data center capacity, servers, network infrastructure, and office facilities, as well as scaling our headcount to support our growth, including in our Reality Labs initiatives, will continue to drive expense growth in 2022. We expect 2022 capital expenditures to be in the range of $29-34 billion and total expenses to be in the range of $90-95 billion

Data and infrastructure cost – To date Meta has invested ~$17B in reality labs against 14 data centers in the US and ~$4.1B against 4 data centers internationally, amounting to ~$21.3B. Meta’s President of Infrastructure & Data Centers, Tom Furlong has stated that they have 48 active buildings and another 47 buildings under construction, signaling 70 additional buildings in the coming years.

Hardware for metaverse AR/VR headsets – Meta acquired Oculus in 2014 for $2B and since has added $250M in the VR upgrades and committed to spending another $250M for future projects. CEO Mark Zuckerberg has committed to spending around $3B in the coming decade on VR-related projects. Meta Platforms has meaningfully accelerated its investments, purchasing 6 VR content studios in the past 2 years.

Workforce – Meta has 10,000 employees working full-time on metaverse-related activities. This represents 1/6 of the Meta workforce. During the last earnings call, management announced its goal to double this by hiring an additional 10,000 employees in Europe for its Facebook Reality Labs segment over the next five years.

Content creators - During the 2021 Connect event, Meta announced that it will create a ~$150mm fund to help train and develop the next generation of creators. In addition to Meta’s ~$150mm VR/AR learning fund for creators, Meta has also recently announced a ~$10mm creator fund to support Horizon. Meta will distribute these funds through community competitions offering up to ~$10k for the top 3 winners, its Creator Accelerator Program which will launch in early 2022, and partnerships for funded opportunities

Goldman Sachs did a comparative study of Meta and other related companies and created a model based on the market cap of all metaverse companies. They concluded the total market cap is ~$12.5T. I did some more research and followed the Grayscale report on the total market cap for web2.0, web 3.0, Facebook, and gaming/eSports companies and they project a total market cap of ~$14T. Statista also projects the total market to be in the range of $14T. Here is the breakdown by Grayscale on the market cap for different sectors. (Link here, pg. 9 of this report)

Assuming Goldman’s number of ~$12.5T, and looking at the private market across gaming, online games, augmented reality, and virtual world categories - during 2021, ~$10.4B of capital has been raised so far across 612 deals (up from ~$5.9B in 2020). Based on this data they plotted the % of market cap and total private funding that is expected to enter the market. (You can read each value as % of $12.5T + Private funding, for example first value of $135B = 1% of $12.5T + $10B). Based on this table we can estimate minimum expenditure of around $135B and a maximum expenditure of around $1.35T.

Goldman estimates this expenditure to be between $135B and $700B.

If we take the market cap of gaming, crypto, and web2.0 metaverse companies of around $14T, this expenditure would be around $800B at the high end. Well, only time will tell how crazy investors go to support the metaverse vision. Now that we have understood of costs associated with building metaverse, let us dive into TAM and understand different factors that will define the TAM.

Total Addressable Market (TAM)

Metaverse, as experts and banks put it, is set to become the next generation platform to replace mobile internet. I expect metaverse TAM to be expansive and go beyond the current online consumption market which is mainly dominated by e-commerce and online entertainment spending. Further, the COVID-19 pandemic has proved to be instrumental in paving the interest for the metaverse. It has speeded up the emergency of the virtual communities as major lifestyle areas for locked-down users including interactive gaming landscape, as well as increasing adoption of mixed reality.

Looking at the numbers, different organizations project a different number in the range of $800B to ~$2.6T. I am going to put the links to different sources below. I do not intend to counter these organizations, but instead, I want to focus on what will constitute business in the metaverse.

Bloomberg – estimates the market size of $800B with 13% CAGR. You can read the report here

Goldman estimates a market size of ~$2.6T. You can read the full report here

Grayscale estimates a market size of ~$1T. You can read the full report here

Like I said, let us not hang on to these numbers and take them with a grain of salt just from the fact that research and understanding of the metaverse’s market are preliminary and speculative at the most. However, it’s more important to understand what are the components that will make the metaverse market and understand the current investment, expenditures, and revenues to estimate and project future outcomes.

It is imperative at this point that I define the components of the market that I am considering as part of TAM. There could be components that y’all could consider that would change the TAM. I am considering the following aspects of the metaverse of calculating TAM.

Virtual reality hardware market

Gaming industry

Social world

Live entertainment

Advertisements

Retail

Education

Looking at this list you should ask where Payment in this list is. Before I provide any explanation let me state that payments (especially decentralized finance De-Fi) will play a huge role in the metaverse, but I believe that it should be analyzed separately in the crypto/Ethereum market. I have considered the transaction and economics of currencies (both crypto and in-game currencies like R$, Roblox dollar) in-game expenditure in this blog later as part of Advertisements and retails.

Hardware market

Is this what recreational drugs feel like – is a line from the movie “Free Guy” by Ryan Reynolds. If you haven’t, you need to check out this trailer

Ryan’s name is “Guy” and is a non-player character. He has these sunglasses/eyewear or augmented reality gear (let’s call them sunglasses) showing in-game content like score, power-ups, loot, etc. Sunglasses are the lens through which players are meant to experience Free City’s metaverse and decode its mysteries. To be clear, Free City is not technically a metaverse; the film’s at-home gamers don't play it in virtual reality headsets. If anything, the game is a stand-in for what it's like to be Very Online: fun, but there’s danger around every corner. For Guy, an NPC, Free City is the whole world; it's as if he lives in a metaverse but has no offline counterpart.

The point of writing on Free Guy is to showcase the importance of these “headgears/sunglasses/AR/VR” or whatever you may want to call them. These devices will be the connection between the physical world and the metaverse.

According to Mark Zuckerberg, in the future, many physical objects (e.g., TV, computers, etc.) can simply be holograms designed by creators and consumers will use AR glasses to optimize the physical world and VR to be fully submerged in the virtual world.

According to Markets and Markets report, the Augmented reality (AR) market is supposed to grow from $15.3B to $77B by 2025 at a staggering 38.1% CAGR. Similarly, the Virtual Reality (VR) market is projected to grow from $6.1B to $20.9B in 2025 at 27% CAGR.

Like what we saw with the mobile internet, consumer adoption of AR & VR will be a driving factor in business opportunities. If we look at the current penetration of the market, we can establish that the metaverse is just getting started and the runway is still big. (See below chart compiled by Goldman to project the AR and VR users, AR is on the left, VR is on the right).

All key players participating to build metaverse into reality understand the need to bridge the technological gap that is currently there with AR/VR. It’s in this spirit that Niantic has joined with Qualcomm to invest in a reference design for outdoor-capable AR glasses that can orient themselves using Niantic’s map and render information and virtual worlds on top of the physical world. Unlike the walled gardens, companies are attempting to create, an open consortium that will enable many partners to create and distribute compatible glasses.

Google in 2017, announced AI-powered Google Lens that provides users with various use cases when the user points the camera at the object. These use cases include translating text with Google Translate, smart text selection (e.g., copy and pasting of Wi-Fi password), smart text search via Google’s search engine, shopping, and searching around you (e.g., providing details of your surroundings such as details on document).

At Google’s annual I/O developer conference, the company announced Multitask Unified Model which will be able to take information across an array of formats (from text to videos to images) and provide a user with an enhanced search result. As an example, you point the Google Lens to a hat you like and ask Google (via text) to find the pattern of the hat but in the form of a shirt. With the Multitask Unified Model combining the visual and text component, Google will be able to provide the user with enhanced search results.

Snap. To date, Snap has 200k Lens creators, developers, and partners building millions of AR experiences, with nearly ~2M lenses created with Lens Studio, and ~2T Lens views with use cases spanning across utility (e.g., taking spatial measurements), entertainment (new form of storytelling for entertainers), shopping (e.g., trying on shoes in AR and purchasing directly), self-expression for creative communication, games allowing multiple players to compete in shared AR gaming experiences, and education

Gaming industry

Before COVID-19, video games were already starting to blur the lines between virtual and physical events & activities as demonstrated by in-game events in Fortnite and Roblox (e.g., Star Wars: The Rise of Skywalker, DJ Marshmello concert, Weezer album debut), professional eSports players partnering with celebrities on Twitch (e.g., Drake and Ninja playing Fortnite), and Take-Two’s online casino in Grand Theft Auto where gamers could gamble real money. As a result of these in-game events and activities, these key franchises saw user base expansion and increased levels of engagement, consumption, and ultimately monetization. And on the other hand, these events allowed content creators to connect with the next generation in a new forum that boasts high levels of engagement. During COVID-19, social restrictions placed an importance on the need to have virtual events and connections, resulting in the social acceptance of virtual existence. During the pandemic, video games, streaming platforms, and communication apps allowed consumers to digitally connect, with canceled in-person graduations ceremonies, weddings, and many other significant life events taking place via Minecraft, Roblox, and other platforms.

Opening new gaming opportunities, removing the barriers

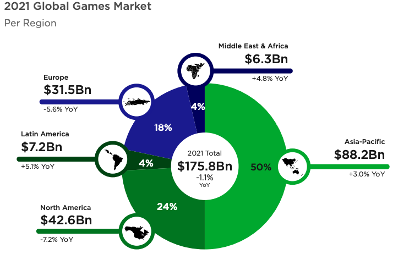

The video game market was around $175B in 2020 and will reach $218B by 2024 according to newzoo, growing 8% CAGR. Current market distribution is shown below:

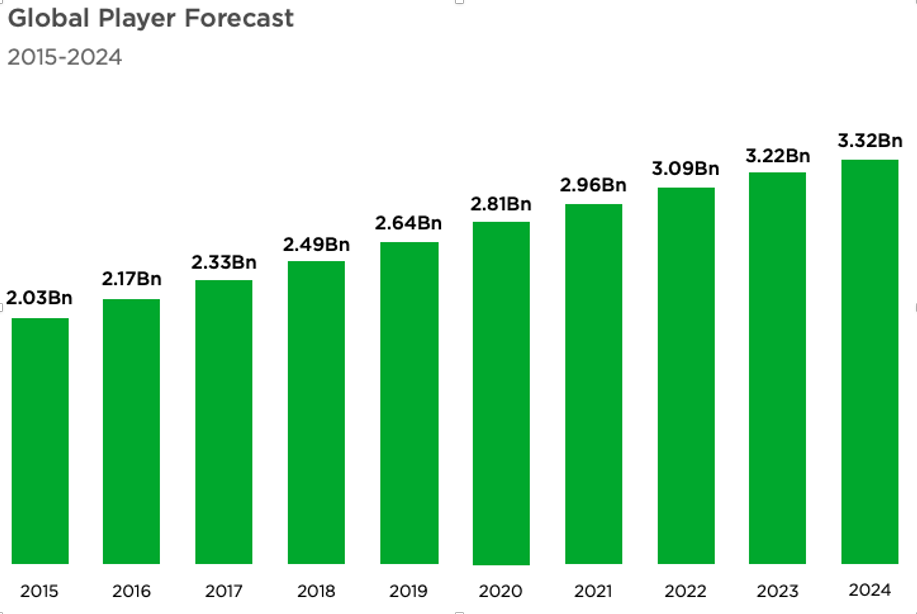

The Asia Pacific will be the biggest market generating almost 50% of the revenue. Among segments, smartphones will be the biggest and fastest-growing segment with revenue generation of ~$94B. Also, the global players will reach 3.3B by 2024 up from 2B in 2015.

The gaming industry is changing and evolving really fast. It is trying to break free of the walled gardens of the traditional gaming organizations to a more decentralized and open environment. If we look at the history of gaming, games were purchased with an upfront fee of $50-$60 with players only allowed to play on a limited platform. This gave Fortnite an opportunity and in 2017 they released free to play Battle Royal game which could be played from any platform. I wrote in Part II of the Metaverse blog, that part of Fortnite’s success came from the struggle to overcome traditional anti-competitive practices by being compatible across devices and operating systems. Rather than locking the user into one console version, you can play Fortnite on virtually any platform today. However, Fortnite has said they will explore a more permission/curated version of NFT like an app store. It also expanded the addressable market and allowed EPIC to create an ecosystem in which they can promote live services (like monetizing skins that have no direct impact on the game) and host virtual events (like the Ariana Grande concert) for gamers and artists to connect. This opened up the competition and what has happened since is that it has allowed the business model to shift from upfront fees to more in-game purchases and hence expanded the use of cryptocurrency. Look at the expenditure on premium games vs in-game spending (developed by Grayscale). This spending will further increase with the on-set of web3.0 and interoperability (see my blog on 3 things required to make metaverse happen), where users will be allowed to transfer NFTs and other digital assets creating an altogether new free-market internet native economy that can be monetized in the free world.

This trend is pushing AAA publishers to focus on in-game content which is showcasing an increase in digital revenue (compared to physical revenue)

Targetting next generation of users

Looking at how the next generation of users spent their digital time in 2020 across the US, UK, Spain, we can see that online video and social media represent ~26% of screen time and gaming falls closely behind at ~22% of screen time. However, when looking at the top apps by time spent, Fortnite and Roblox rank first and second with more than an hour and a half spent in the games, both of which are open environment multi-player games, signaling the value the younger generation places on social elements and virtual worlds within gaming. This research was conducted by Qustodio (you can read the full report here) and data compiled by Goldman (see charts below, pg 12 of the linked document here).

It is alarming to see the increasing level of screen time among kids or should we say the generation that will be the prime user of the metaverse. Covid-19 propelled screen time by almost 100% as everything from education to play, socialization, and even exercise was forced online. The kids were literally trapped behind the screen. Propelled by this demand, stream giants like YouTube, Netflix, Disney, etc. pushed enormous content. As a result, the consumption increased too, and it increased across kids as well. As I stated earlier metaverse is at least 10-15 years out, companies like Roblox, Fortnite, YouTube, etc. are creating products for the future army, preparing them for a virtual future. Right or Wrong is debatable.

Investing in a virtual experience

According to Newzoo, for gamers choosing their avatar’s physical abilities/appearances is key in terms of driving the overall gaming experience within the metaverse. Roblox is a critical player in metaverse gaming and has understood this need from its users. It is investing heavily in users’ virtual experiences. Roblox currently has ~47M DAUs (also per Roblox investor relation page) and is projected to reach ~78M by 2024 which will consume approx. 2.5 hours per day of gamers’ time. Roblox plans to expand in developing R$, its currency which can be used to customize avatars, or used to acquire development resources. Further, their strategy includes allowing individual content creators, video game studios, movie studios, and music studios to create a non-gaming environment.

Roblox will monetize these experiences, currently, ~25% of their revenue comes from the marketplace. Avatars are the major drivers of the marketplace, almost 20% of the gamers change their avatars daily. As I stated above supporting user-generated content will be a major driver in Roblox’s success. At this moment they have around 500 UGC developers who launch 350 items per week and 65% of these items are sold out. UGC model has accelerated and shown Roblox the future direction to monetize this space.

Like Roblox, you can imagine how other companies dreaming about metaverse, plan to decentralize the model whereby various brands and creators can build their store sell virtual goods to consumers to further build out their virtual identity. Recently, on Feb 16th, JP Morgan opened the onyx lounge in decentraland.

Here, you can see how Roblox avatars have changed over the years, just for quick comparisons. First Image (2006-07) and Second Image (2021 - Present)

Newzoo conducted a survey asking a question “How good or bad do you think each of the following content and features would be, in terms of your overall enjoyment?” On the left you can see the mean results of the survey out of 7

Social World

Live Entertainment

Web 2.0 has allowed companies like Roblox and EPIC to create virtual metaverse kinds of experiences. Like Fortnite hosted an in-game concert with DJ Marshmello which had ~11M visitors and nearly ~27M views on YouTube.

Since then the partnership model between brands and “metaverse type” companies has started. Here you can see the list compiled by Goldman Sachs for such events.

Driving engagement with virtual events will be the key to success. It will be the new way to connect artists to their fans and vice versa. Some of these ways include virtual concerts, launch parties, listening parties. In 2021, Roblox organized a listening party for musicians which can build on launch parties and artists can release a new album. Partnering with Roblox, Grammy-nominated artist Poppy released a new album in 9 Roblox experiences (4 of which had 3B lifetime visits).

Animoca brands subsidiary The Sandbox blockchain is partnering with warner music group to create a combination of musical theme parks and music venues. With the deal, we could see metaverse performances from some artists signed to its labels, including Atlantic, Warner Records, Elektra, and Parlophone. But there’s no guarantee of appearances. The Sandbox already has more than 200 existing partnerships, including with Snoop Dogg, Steve Aoki, Adidas, and Atari. In November 2021, The Sandbox raised $93 million in Series B funding from a high-profile list of investors, including SoftBank Vision Two Fund, Galaxy Interactive, Thai bank subsidiary SCB 10X, LG Technology Ventures, and Samsung Next.

Retail, Properties and Advertisements

When I say advertisements, it is more like brand integration. I talked briefly about JP Morgan opening the onyx lounge in decentraland. Other partnerships are emerging to connect with a large and engaged user base through an immersive experience. With the advent of web 3.0, the ownership structure in virtual economies is changing. Decentraland which is an Ethereum-based platform the average price of the parcel of land has doubled in 2021. $12,000 is the average price of a parcel of land which is 100% more than what it was 6 months ago. In June 2021, one land package in Decentraland was sold for $913,000, with the developer Every Realm (formerly Republic Realm) turning it into an entire shopping district, Metajuku (inspired by Japan’s Harajuku shopping district). Brands are going directly to developers to promote physical experiences and products. Here are a few key examples of how this works.

Prager Metis International LLC, a New York-based accounting and advisory firm opened a virtual three-story property on a site it bought for nearly $35,000 in late December. Prager Metis plans to use its virtual building to advise companies and other new and existing clients on tax and accounting issues. The firm expects that many of its clients, particularly those in the entertainment and fashion industries, will seek its services in the metaverse as more companies decide to conduct business there.

Gucci Garden: Gucci partnered with Roblox to create a Gucci Garden which had a store, museum, and restaurant. Nearly ~20M visited and someone bought a virtual Queen Bee Dionysus bag for $4115 compared to a real market price of $3400. While the launch price was $6 but seeing the scarcity around this bag the bidding quickly escalated to $4100.

Chipotle: In Oct 2021, Chipotle partnered with Roblox to provide the first 30,000 visitors with a chipotle inspired costume and a free burrito coupon. The Roblox/Chipotle partnership represents Roblox’s first food-related partnership, signifying the many use cases that Roblox can offer.

Vans World: In Sept 2021, Vans partnered with Roblox to create a Vans World like Gucci Garden. It had ~48M visitors and has allowed vans to generate an additional source of revenue.

Nikeland: Nike created this bespoke world with the backdrop of its world headquarters and inside Roblox’s immersive 3D space, building on its goal to turn sport and play into a lifestyle. Few things to know about Nikeland:

NIKELAND is enhanced by real-life movement, encouraging visitors to get more active

The digital showroom allows you to outfit your NIKELAND avatar with special Nike products

NIKELAND is free for anyone to visit and experience on Roblox, breaking down one of the biggest barriers to sport — access

The digital world will come to life at Nike’s House of Innovation (HOI) in New York City via Snapchat

JP Morgan estimates the total in-game spending in metaverse will reach $18.41B. Virtual concerts have the potential to be more profitable than physical concerts, which deal with barriers such as capacity and parking. Recently, a major concert held in Fortnite was seen by 45 million people and grossed around $20 million, including sales of merchandise. It will be interesting to see how marketing pans out for the digital world and has the potential to be one of the biggest revenue generators for metaverse (or meta-economy). As with the current generation, social media companies have realized advertising the model to generate revenue.

Education

Education opportunities are going to expand with VR being the low-cost and effective way to access training. Roblox has an education platform focused on students and educators in STEM curricula. Roblox has 240+ organizations teaching in Roblox studio in 74 countries. Roblox created “Learn and Explore” which allows developers to build their own games featuring experiences. As of Sept 2021, Roblox had 7M+ monthly users in the education experience.

Here are some of the use cases for education utilizing metaverse

Instructors can create rooms with life-like objects

Instructors and students can use ultra-realistic avatars

Read this article from Verge - Amid the fluff, Meta showed an impressive demo of its Codec Avatars

Organizing student study groups and conducting faculty meetings

Students can build study rooms to meet

Building on the points above, the ability to see and speak to one another in realistic environments helps create a sense of community through genuine interactions and communication.

Incorporating education in the Metaverse allows students to collaborate, socialize, and play games in class

Instructors have different ways to connect with students such as speaking and seeing each other, holding office hours, sharing files and resources, networking, and even playing games.

Computer science where students can earn badges for introductory coding

Foreign languages where they can be part of a team who learns the newest words in a week

Anatomy (a new twist on the knee bones connected to the thigh bone)

Military history where they can imagine themselves in the shoes of famous generals

Accounting where students' “learning accounts” grow as they master each facet of the material

While studying for this article, one thing that I have realized is the importance of interoperability whereby consumers can seamlessly take virtual assets and experiences through a metaverse. Although metaverse is still in its infancy, the infrastructure is being built piece by piece. What we need are the social attitudes to change to experience this new era on the internet.

What we need are the social attitudes to change to experience this new era on the internet

To make metaverse ubiquitous, early-stage investments are emerging across multiple themes including social media, video games, e-commerce, and blockchain.

At the heart of the opportunity are the social media and video game companies leveraging their large user bases, creator platforms, experiences with live digital events, and cutting-edge hardware to build the foundations of the metaverse. Beyond that, powerful e-commerce firms are likely to benefit from new sales channels and features, while blockchain companies are likely to be essential in providing the financial infrastructure underpinning the metaverse economy.

Roblox, Microsoft (Minecraft + Activision), and Epic Games’ Fortnite appear to be early leaders in the race for Metaverse leadership but there’s ample time for other game makers and social networking companies to tweak existing services or launch new ones to capitalize on the market’s growth. Other game makers have been able to attract large, active user bases in online titles such as EA’s the Sims, Take-Two’s GTA Online and Nexon’s MapleStory, and Dungeon&Fighter Online. These companies could seek to add additional social features and make user-generated content to become a larger part of their experiences to capture Metaverse demand.

There is still a lot to unpack. Watch out for this blog to get the latest info on metaverse and other topics. Please subscribe to get the content delivered directly to your inbox.

Cheers